Do you Rating a Va Financial Which have a four hundred Borrowing Score?

Dating site one specialize in Puerto Rico brides

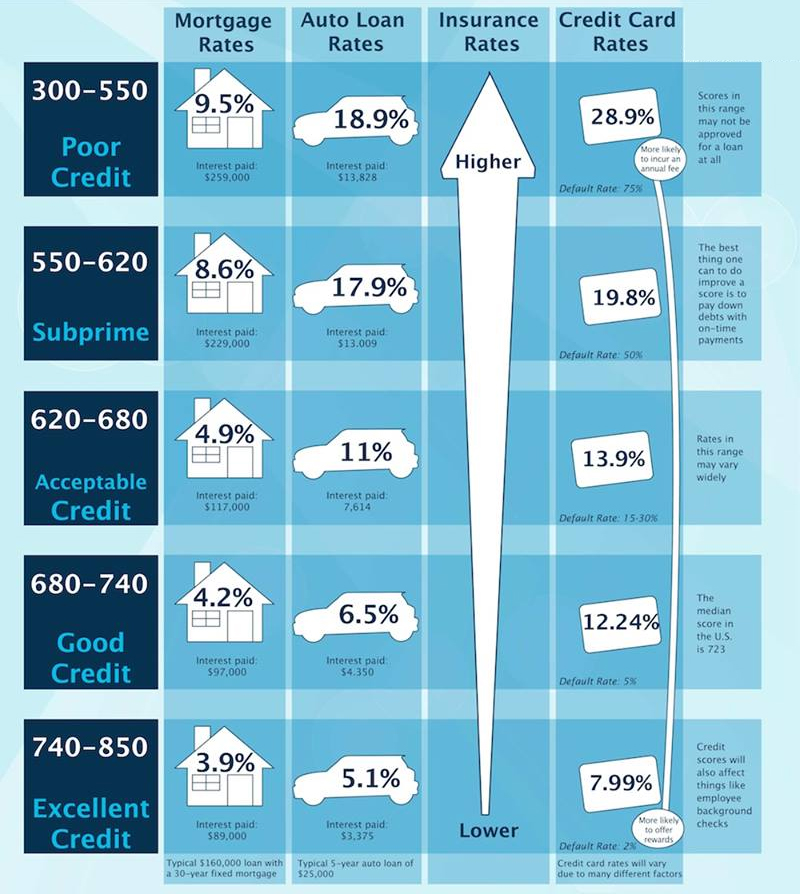

October 2, 2024A credit score shows lenders how good you do borrowing

October 2, 2024Desk away from Material

Va funds (supported by the brand new Department out-of Experts Products) is a kind of mortgage offered to current and earlier in the day solution players. The latest Va by itself cannot mortgage the cash but instead guarantees a fraction of they when you find yourself Va-acknowledged traditional lenders finance the borrowed funds.

Virtual assistant financing promote specialized programs and you can guidelines to own pros and regularly have more easy conditions to have certification than just a classic financing. Regarding lower down costs to a higher money-to-personal debt proportion demands, a good Virtual assistant financing can sometimes be simpler to and obtain possesses even more attractive words than antique lenders regarding home purchases.

What is actually experienced bad credit?

There isn’t any agreed-through to definition of bad borrowing from the bank, just like the each financing agencies features its own translation, https://paydayloansconnecticut.com/ridgebury/ and loan providers will at the a range of results. Credit reporting agencies typically break out credit ratings into the four brackets that have rough results below:

- Excellent: more 720, otherwise both over 750

- Good: lowest 700’s

- Fair: mid in order to upper 600’s

- Subprime: lower 600’s

Brand new Virtual assistant by itself will not stipulate the very least credit score, however the loan providers they work which have would, and people may differ. It is essential to keep in mind that loan providers are thinking about significantly more than simply your credit score, thus regardless if your own is in the Fair to help you Subprime diversity, will still be you’ll be able to in order to harmony they together with other activities.

Aside from the credit history, precisely what does the latest Va envision?

Virtual assistant money are made which have veterans’ certain needs in mind, comprehending that solution participants could deal with better financial hardships than just their civilian alternatives. Thanks to this, he is offered to playing with most other bits of your financial history to utilize due to the fact equity for your creditworthiness. Other places they could thought include:

Rent and you can home loan record

It is almost always checked along with a cards get. Whether you are to shop for a home otherwise refinancing, as much as possible let you know several+ weeks out-of into-big date book otherwise mortgage repayments, it helps combat a lesser credit rating.

As well as lease and you will mortgage repayments, loan providers also evaluate constant payments instance college loans, automobile costs, or personal credit card debt. They are going to like to see which you have generated uniform costs more than an excellent several-week background, without missed otherwise later repayments.

For those with property foreclosure and you can/Otherwise case of bankruptcy

It’s still you’ll be able to to be eligible for an effective Virtual assistant loan if you’ve gone through bankruptcy proceeding otherwise foreclosure. If you’ve gone through Chapter thirteen Personal bankruptcy you’re going to have to inform you at the least 12 months of with the-big date percentage background becoming experienced. That have Chapter 7 Bankruptcy proceeding, you’ll have to show at the very least 2 years off into-date commission record. As a whole, you will need to hold off a couple of years just after a property foreclosure to utilize getting an excellent Virtual assistant mortgage.

CAIVRS background

CAIVRS is the Credit Alert Interactive Confirmation Reporting System. The program investigates the loan condition which have people previous federally-helped money. If the talking about not paid up to date, you may not qualify for an effective Va loan. So it organization was independent regarding a classic credit rating institution since it doesn’t eliminate studies out-of personal loan providers instance credit cards or auto loans, and you may rather looks at such things as SBA loans, Dept. regarding Studies finance, and you can DOJ judgments.

Va loans you should buy which have poor credit

Despite less than perfect credit, it’s still it is possible to to help you qualify for an excellent Va loan. It could be more complicated, and there are certain facts you ought to be aware of:

It’s harder locate home financing without advance payment for those who have bad credit. Overall, you will need a get of around 640, however, based the Va entitlement finance, you may still have the ability to meet the requirements that have a lower score. The brand new Va insures your loan to loan providers in the event that you default or enter into property foreclosure. Extent they ensure is known as the new entitlement.

Typically loan providers have a tendency to approve a no-down-fee mortgage if the overall amount borrowed is actually five moments the fresh entitlement (For example: the entitlement is commonly 36K, so you could be eligible for a good 144K loan and no off payment). The new experts at Champion House Apps can help demand a certification away from qualifications to determine your own accurate amount.

Refinancing money

Refinancing funds is actually checked-out the same way once the an alternative buy financing regarding the attention from a lender, but you can find two things you will need to believe whenever applying for a refinancing mortgage which have bad credit:

- Loan providers could possibly get improve settlement costs in order to counterbalance a diminished credit history, and Va caps closing costs within step 1% of your buy well worth. Particularly, whenever you are borrowing 200K plus closing costs surpass $2,one hundred thousand, you will possibly not qualify for Virtual assistant resource.

- In the event the settlement costs was rolled for the loan, you need to reach your split-actually area-extent you save each month through the elimination of the monthly payments talks about the entire closing costs-within 3 years. If you’re significantly out of this period of time, you will possibly not qualify.

Virtual assistant IRRRL

Va IRRRL, brief for Rate of interest Avoidance Refinance Finance, are only to have refinancing and never purchasing and are generally readily available just from the Virtual assistant. With this particular financing, you don’t need an assessment but will need to show a dozen+ weeks out-of with the-date home loan repayments. You are also in a position to roll the brand new closing costs to the amount borrowed cutting your out-of-pocket can cost you.

Contact us today!

Basically, sure, you can aquire an excellent Va mortgage having a decreased credit score. Is it more complicated? Sure, but don’t help bad credit prevent you from looking at a great Virtual assistant financing. Discover formations in position to greatly help, and be blown away within what you are actually qualified to receive.

This new gurus within Character Home Applications will help you discover local lenders, offers, and you will rebates to help you get on the home you are entitled to, despite poor credit. Book a scheduled appointment now and start on the way to homeownership the next day.