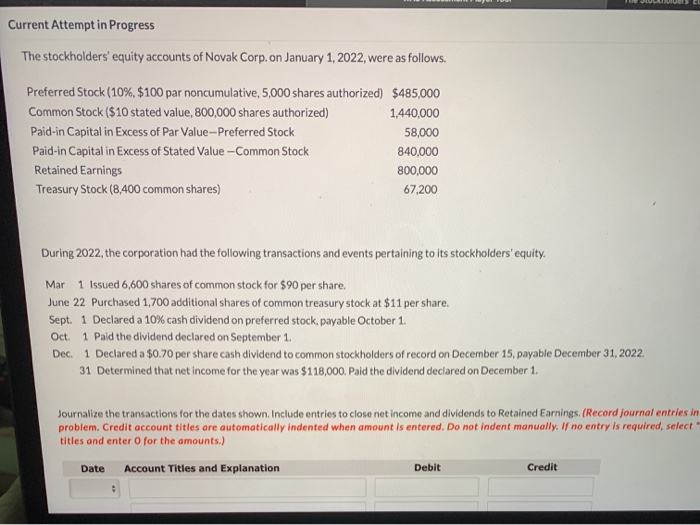

5 9 Treasury Stock Financial and Managerial Accounting

Price Aion AION today Market cap, charts, exchange rates.

January 12, 2022Las 10 mejores herramientas de desarrollo web

January 13, 2022

The Cash accountincreases with a debit for $45 times 1,000 shares, or $45,000. ThePreferred Stock account increases for the par value of thepreferred stock, $8 times 1,000 shares, or $8,000. The excess ofthe issue price of $45 per share over the $8 par value, times the1,000 shares, is credited as an increase to Additional Paid-inCapital from Preferred Stock, resulting in a credit of $37,000. When a company issues new stock for cash, assets increase with adebit, and equity accounts increase with a credit.

Share This Book

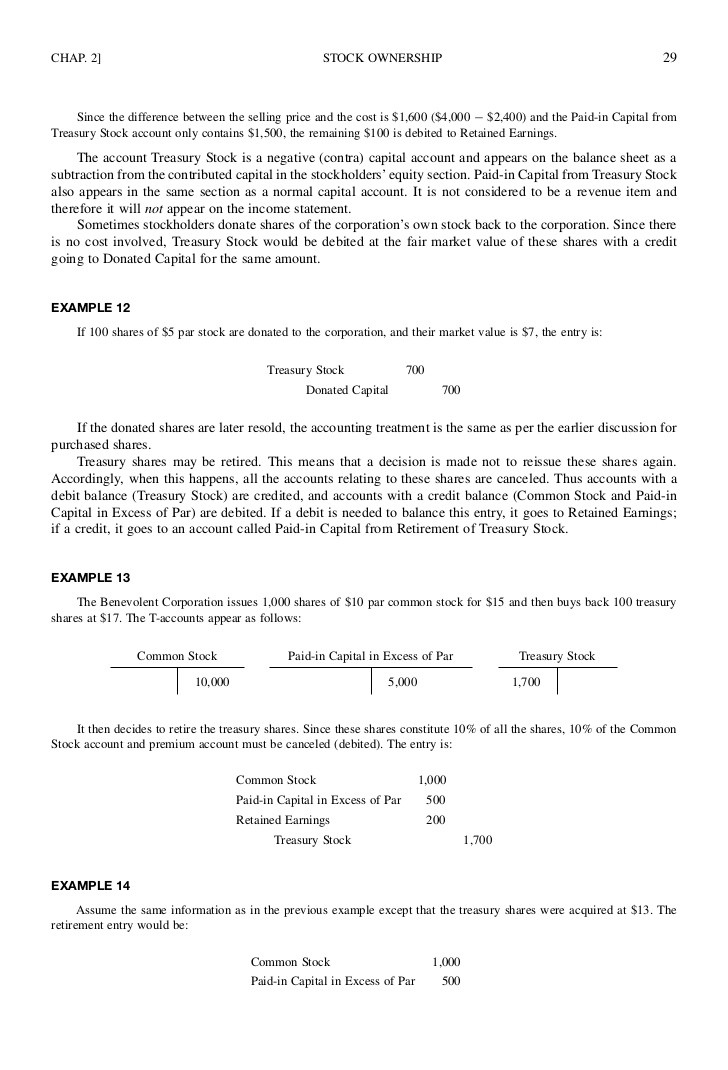

Treasury stock transactions can only reduce the retained earnings of a company and cannot increase them back. Treasury stock is an account created for any shares that are repurchased by a company only if the company intends to resell those shares. If the company plans to retire these shares, treasury stock accounts are not created.

What effect does the sale of treasury shares below the original purchase price have on assets and retained earnings?

Common Stock consists of the par value of all shares ofcommon stock issued. Additional paid-in capitalfrom common stock consists of the excess of the proceeds receivedfrom the issuance of the stock over the stock’s par value. When acompany has more than one class of stock, it usually keeps aseparate additional paid-in capital account for each class. Under the par value method, at the time of share repurchase, the treasury stock account is debited, to decrease total shareholder’s equity, in the amount of the par value of the shares being repurchased. It is common for stocks to have a minimum par value, such as $1, but sell and be repurchased for much more.

Q. Is Treasury Stock the same as outstanding shares?

Under par value method, purchase of treasury stock is recorded by debiting treasury stock by the total par value of the shares. Cash account is credited for the actual amount paid to purchase the treasury stock. Any additional paid-in capital or discount on capital relating to treasury shares is cancelled by a debit or credit respectively. At this point, if the sum of credit side of the journal entry is less than the sum of debit side, additional paid-in capital account will be credited for the difference.

Does APIC only record the additional paid-in capital from shareholders?

- The effect of the transaction is to reduce both assets and stockholders’ equity by $24,000.

- However, the more prevalent treatment in practice has been for all outstanding options – regardless of if they are in or out of the money – to be included in the calculation.

- Corporations may choose to hold treasury stock to raise capital later through resale, to boost shareholder interests, or to retire them completely.

- The percentage of profits or losses attributable to a single partner is decided when the partnership agreement is signed.

- For example, as of the end of FY 2023, Apple Inc. (AAPL) had total assets of $352.58 billion and $290.44 billion of total liabilities.

- Upon reissuance, any amount received in excess of the carrying amount of the treasury shares must be credited to the Capital Stock account.

The company may also choose to reacquire its shares through a tender offer to its shareholders. In this method, the company offers it shareholders to sell their shares back to the company at a specified date and price. Any shareholders that are willing to take up the offer submit their application for their shares to be reacquired. Companies may also choose to give a Dutch auction tender offer to their shareholders. In this method, the company offers it shareholders a range within which they can bid to sell their shares.

What is the approximate value of your cash savings and other investments?

As this partial balance sheet shows, treasury stock is not shown as an asset but as a negative item in stockholders’ equity. The effect of the transaction is to reduce both assets and stockholders’ equity by $24,000. When a company issues stock for property or services, thecompany increases the respective asset account with a debit and therespective equity accounts with credits. Chad and Rick have successfully incorporated La Cantina and areready to issue common stock to themselves and the newly recruitedinvestors. Thecorporate charter of the corporation indicates that the par valueof its common stock is $1.50 per share. Stock with no par value that has beenassigned a stated value is treated very similarly to stock with apar value.

However, it may indirectly benefit shareholders by potentially boosting EPS and share prices. Under the cash method, the treasury account would be debited for $50,000 and cash credited for $50,000. Corporations use buybacks to reduce the amount of shares in circulation, thereby boosting their stock price.

If treasury stock method is used, any purchase of treasury shares results in a credit to APIC and a debit to treasury stock at cost. The two aspects of accounting for treasury stock are the purchase of stock by a company, and its resale of those shares. In the subsequent step, the what is form 720 where to get how to fill out TSM assumes the entirety of the proceeds from the exercising of those dilutive options goes towards repurchasing stock at the current market share price. The assumption here is that the company would repurchase its shares in the open market to reduce the net dilutive impact.

The following journal entry is recorded for the purchase of the treasury stock under the cost method. Treasury stock at cost method is an accounting approach by which the actual price paid for treasury shares are debited to APIC and credited to treasury stock at cost. The difference between the actual price paid and the par or stated value of treasury shares is recorded in an account known as gain or loss on purchase and sale of stock. Notice on the partial balance sheet that the number of common shares outstanding changes when treasury stock transactions occur. The 800 repurchased shares are no longer outstanding, reducing the total outstanding to 9,200 shares. The treasury stock method is an approach companies use to compute the number of new shares that may potentially be created by unexercised in-the-money warrants and options, where the exercise price is less than the current share price.

Retired shares will not be listed as treasury stock on a company’s financial statements. Under the par value method, the treasury stock account is debited to decrease total shareholders’ equity at the time of share repurchase. This is done in the amount of the par value of the shares being repurchased. When it comes to accounting for treasury stock, there are two methods that can be used. These methods are the cost method and the par value method of treasury stock. The cost method and par value are used on the assumption that the shares that have been reacquired will be resold in the future.

These may include forms such as sole proprietorship, partnership or company. The single owner invests in the business initially and owns the business until the business is sold or another owner joins the business. Our accounting firm is a professional service firm that focuses on providing expert advice in accounting and tax. They are able to provide our clients with the most accurate and reliable solutions for their particular financial/accounting needs.